Repensando as agências bancárias: uma abordagem de três pilares para a transformação

julho 13, 2024 / Satya Swarup Das

O sistema bancário está em sua era "figital". Ao preencherem a lacuna entre as ofertas e capacidades físicas e digitais, os bancos estão em busca de maneiras de atender às necessidades e expectativas dos clientes. E isso significa mudanças.

Mas essas mudanças estão por vir há muito tempo. A preferência dos clientes pelos canais digitais reformulou a maneira como as agências tradicionais estão se adaptando a essa nova realidade. Anteriormente, as agências atendiam principalmente clientes com foco transacional. Os clientes iam até as agências físicas em busca de garantia e assistência personalizada, o que os canais digitais não podiam fornecer. No entanto, uma mudança radical rumo aos canais digitais obrigou os bancos a reimaginar suas ofertas. Essa mudança interrompeu o equilíbrio entre canais digitais e de agências, forçando os bancos a repensarem suas estratégias de atendimento físico.

Isso não quer dizer que todos os clientes tenham conhecimento digital; muitos ainda dependem de interações presenciais, especialmente para interações complexas, incluindo aplicação hipotecária ou planejamento financeiro. De acordo com uma pesquisa recente do Banking Outlook realizada pelo BAI[1], os clientes esperam fazer cerca de 60% de seus negócios bancários digitalmente até 2024, deixando cerca de 40% ainda exigindo interações presenciais.

Embora os bancos maiores tenham iniciado sua jornada para encontrar o equilíbrio certo entre ofertas digitais e físicas, outros ainda estão descobrindo o melhor modelo para atender às necessidades dos clientes e permanecer competitivos. A seguir estão as estratégias práticas que os bancos podem empregar para encontrar o equilíbrio certo entre ofertas digitais e de agências. Descubra a abordagem de três pilares para ajudar suas operações bancárias a evoluir para melhorar a experiência do cliente e impulsionar o crescimento.

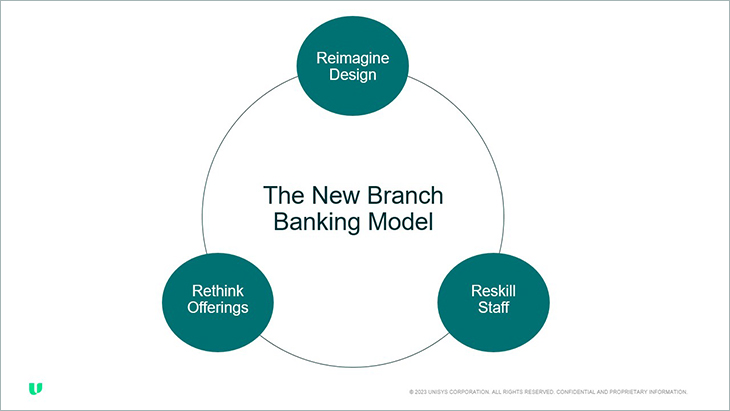

Conheça o novo modelo de agências bancárias

Pilar 1: Reimagine o design

O primeiro pilar deste novo modelo exige que as agências evoluam para se tornarem centros de experiência do cliente, em vez de centros de realização de transações. É possível transformar o ambiente físico substituindo balcões individuais tradicionais por balcões flexíveis que atendam a diferentes necessidades dos clientes. E se os funcionários forem equipados com tablets, poderão se mover pela agência, o que permitirá interações interativas e personalizadas com os clientes.

Ao transformar as agências em centros de experiência, é possível oferecer uma mistura equilibrada de experiências digitais e presenciais. Lounges interativos com funcionários equipados com tablets e quiosques de autoatendimento para clientes oferecem um ambiente no qual os clientes podem explorar ofertas digitais enquanto recebem assistência personalizada. Essas interações casuais e experimentais podem ajudar a equipe a abordar de forma abrangente as necessidades dos clientes.

Precisa de mais inspiração? Imagine substituir os balcões tradicionais de suas agências por estações de trabalho colaborativas, em que clientes e funcionários podem se envolver em discussões personalizadas sobre metas e soluções financeiras.

Pilar 2: Repensando as ofertas

E se as agências pudessem se concentrar em fornecer serviços de consultoria e aproveitar a tecnologia para melhorar as experiências dos clientes em vez de simplesmente processar transações? Os bancos podem aproveitar insights de clientes, soluções baseadas em fluxo de trabalho digital e ofertas virtuais para promover um novo nível de experiência em suas agências. Sistemas impulsionados por IA que fornecem uma visão holística do cliente podem permitir que a equipe responda a consultas, ofereça aconselhamento personalizado e oriente os clientes para as soluções financeiras mais adequadas.

Revitalizar sua abordagem também pode eliminar uma das partes mais incômodas da experiência do cliente: a espera. Os agendamentos digitais e a pré-atribuição da equipe a intervalos de tempo específicos podem reduzir os tempos de espera e a ansiedade do cliente.

Imagine o seguinte: um banco introduz suporte virtual a hipotecas e aplicações de empréstimos de forma que os clientes possam se conectar com especialistas por meio de videoconferência dentro da agência.

Pilar 3: Treinamento de pessoal

Um dos aspectos mais importantes da evolução do ramo bancário são as pessoas. Para que qualquer novo modelo de negócios funcione, a equipe da agência deve mudar de uma mentalidade de processamento de transações para se tornar especialista em interação com o cliente. Para isso, os bancos poderiam priorizar a flexibilidade da equipe, oferecendo horários de trabalho variáveis, folgas e oportunidades de aprendizado e treinamento. Funcionários felizes significam clientes felizes. Garantir a satisfação da equipe e melhorar a experiência dos funcionários se traduzirá em clientes mais felizes e melhores experiências para os clientes.

Como isso funciona? Um banco investe em programas de treinamento abrangentes que capacitam a equipe da agência com conhecimento avançado de produtos, habilidades básicas e experiência em sistema bancário digital. Isso permite que a equipe lide com múltiplos produtos e oriente os clientes ao longo de sua jornada bancária, criando uma experiência de cliente perfeita e personalizada.

Colocando o modelo em ação

Os bancos devem começar com um exercício de planejamento abrangente para implementar com sucesso esse modelo de três pilares que envolve considerações de alto nível, como:

- Revisar os serviços e procedimentos atuais

- Encontrando o melhor equilíbrio entre ofertas baseadas em agências e on-line

- Reimaginando o cenário da agência

A implementação de uma nova abordagem leva tempo e, mais importante, requer o acordo das partes interessadas. Uma vez concluídas as fases de planejamento e reformulação, os bancos devem analisar os níveis de habilidade necessários para executar o novo modelo de agências de forma eficaz. Essa análise decidirá se a requalificação da equipe existente ou a contratação de novos talentos deve estar alinhada com o plano de ação.

Garantir a implementação bem-sucedida das mudanças recomendadas requer planejamento cuidadoso e um compromisso com a economia de custos e melhorias de eficiência. Além disso, também há oportunidades para que os bancos gerem mais receita. À medida que os clientes experimentam um melhor serviço, conveniência que economiza tempo e experiências aprimoradas, eles têm mais probabilidade de pagar por serviços e ofertas selecionados.

Redefinindo a experiência da agência para um mundo com digital em primeiro lugar

A era "figital" desafiou os bancos a encontrar o equilíbrio certo entre ofertas digitais e físicas. Ao reimaginar o design das agências, repensar as ofertas e requalificar a equipe, os bancos podem melhorar a experiência do cliente e permanecer competitivos no cenário bancário em evolução.

Com foco em uma estratégia digital em primeiro lugar e um toque humano, os bancos podem transformar suas agências em centros de experiência envolventes que combinam a conveniência dos canais digitais com a garantia de interações presenciais.

Ao adotar esse novo modelo de agências bancárias e aproveitar tecnologias inovadoras, os bancos podem atender às expectativas em constante evolução dos clientes e impulsionar o crescimento e a diferenciação em um setor em rápida mudança. É hora de os bancos abraçarem o futuro do sistema bancário e redefinirem a experiência das agências para um mundo com o digital em primeiro lugar.

Porém, cada banco é diferente e precisa descobrir sua abordagem única. Procurar por ajuda de fornecedores experientes e especialistas do setor e conduzir benchmarking do setor pode ajudar a calibrar suas novas ofertas com as melhores práticas.

A Unisys pode ajudar as instituições financeiras em sua jornada de transformação. Como fornecedor confiável de soluções bancárias de filiais, centrais e digitais, a Unisys pode ajudar você a alinhar suas necessidades com produtos e serviços que atendam às necessidades únicas de cada banco.